Global Pet Insurance Market: An Overview

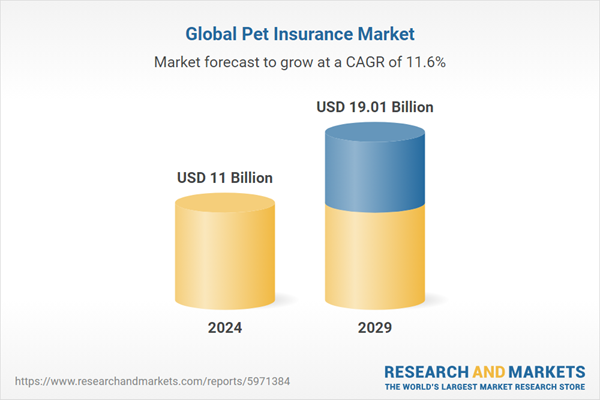

The global pet insurance market is experiencing substantial expansion. In 2023, the market was valued at $9.86 billion, with projections estimating it will reach $19.01 billion by 2029. This represents a compound annual growth rate (CAGR) of 11.56% between 2024 and 2029.

Key factors such as increasing disposable incomes among pet owners, climbing veterinary care expenses, and a rise in pet ownership are major drivers of the pet insurance industry. The introduction of specialized insurance products and pet insurance as a perk in employee benefits also contribute to the growth.

This figure is representative of the growth of the global pet insurance market.

Market Segmentation Insights

By Animal

Dog insurance currently holds the largest share of the market. This is due to the high number of dogs owned globally and their increased need for medical attention. However, cat insurance is predicted to be the fastest-growing sector. This is because cats are increasingly viewed as family members, leading to increased demand for their medical coverage. Also, cats tend to have long lifespans, increasing the likelihood of age-related health issues.

By Policy Coverage

The Accident and Illness segment leads the market in terms of the highest share and is expected to be the fastest-growing segment. These policies cover accidental injuries, illnesses, and sometimes preventative measures. As veterinary costs increase, pet owners better understand the benefits of insurance.

By Provider

The private sector leads the market in terms of the highest share. These providers offer more customizable plans. Additionally, private providers have more resources to invest in marketing and technology.

By Sales Channel

The Direct segment holds the largest share because it allows companies to reduce costs and offer more personalized services. Technological advancements have made it easier for pet owners to compare and buy insurance online.

Regional Analysis

Europe dominates the pet insurance market, with notable contributions from the UK, Germany, and France. The increasing number of pet owners in Europe, coupled with a high rate of pet insurance adoption, fuels its dominance. In 2022, Europe had 340 million pets, including 127 million cats and 104 million dogs, showing strong demand for insurance.

The Asia-Pacific region is the fastest-growing market, driven by factors such as rising pet adoption rates and economic development. Increased awareness of pet health and improvements in veterinary infrastructure also fuel market growth. In India, the market is expanding quickly, with leading insurance companies enhancing their pet insurance products to make them more accessible.

Competitive Landscape

The global pet insurance market is characterized by fragmentation, featuring numerous large and medium-sized players. There is also a significant presence of regional market players.

Key players include, but are not limited to:

- Anicom Holdings

- MetLife

- Trupanion

- Direct Line Group

- DFV Deutsche Familienversicherung

- Animal Friends Insurance Services

- Agria Pet Insurance Ltd

- Nationwide Mutual Insurance

- Pumpkin Insurance Services Inc.

- Figo Pet Insurance, LLC

- Embrace Pet Insurance Agency

- Healthy Paws Pet Insurance

- PetFirst Insurance

Conclusion

The pet insurance market presents a promising landscape, driven by various factors such as growing pet populations and increasing awareness of pet health. With the market expected to almost double by 2029, the industry offers significant opportunities for stakeholders.