Published March 3, 2025

By Lindsay Fenlock, Senior Researcher at the Center for International Environmental Law, and Charles Slidders, Senior Attorney, Financial Strategies at the Center for International Environmental Law, and Nikki Reisch, Director of the Climate & Energy Program at the Center for International Environmental Law.

This is the fifth analysis in a series exploring the intersection of the climate emergency and the insurance crisis.

The destructive wildfires that ravaged Los Angeles in January, displacing hundreds of thousands, have been contained. However, they ignited a different kind of firestorm – one centered on the insurance industry and its increasingly limited coverage of climate-related risks, specifically extreme wildfires.

Climate change significantly increased the likelihood and severity of these fires, which stand among the most destructive in the city’s history. The blazes claimed at least 28 lives and obliterated approximately 16,000 structures across nearly 50,000 acres – an area larger than San Francisco. Insured property damage alone is projected to reach $40 billion, raising the critical question: who bears the cost?

For at least half a century, the insurance sector has understood the physical risks of climate change and the overwhelming responsibility of greenhouse gas emissions, mainly from fossil fuels, in driving rising temperatures. Despite this, US insurance companies hold over $500 billion in fossil fuel-related assets. Moreover, major insurers continue to heavily focus their underwriting business on the fossil fuel sector, with the top US insurers of fossil fuel businesses earning $5.2 billion from underwriting in 2023.

After years of collecting premiums from homeowners and investing significant portions of that money into the fossil fuel industry, which exacerbates climate change, private insurers, such as State Farm and Berkshire Hathaway, have either excluded fire coverage from their policies or completely withdrawn from the California market. In essence, these insurers, who played a role in enabling the very climate disasters now affecting their former customers, have abandoned their responsibilities, leaving residents and the state to absorb the impact.

Private insurers will largely avoid the full financial burden by transferring their exposure to extreme climate risks onto California’s insurer of last resort – the FAIR Plan. By abandoning the California home insurance market or excluding fire coverage, private insurance companies have effectively passed the responsibility of climate risk onto the public while protecting their own profits. Despite their claims to the contrary, insurance companies, as of 2023, continued to generate significant profits on homeowner insurance policies and are reaping record profits.

The FAIR Plan is now on the verge of insolvency. To address the shortfall, the California Insurance Commissioner has levied an assessment of $1 billion on private insurance companies. However, these private insurance companies will pass $500 million of this assessment onto all of California’s insured homeowners. This $500 million bill is a direct consequence of climate change and the profit-driven insurers who have profited from ever-increasing premiums and investments in the fossil fuel sector before abandoning policies for homes most vulnerable to climate risks. All of California’s home insurance policyholders are, in effect, victims of fossil-fueled climate change.

The Anatomy of the LA Wildfires

The LA wildfires’ devastating force is a direct result of climate change-induced drought, which caused an accumulation of dry vegetation and created optimal conditions for extreme wildfires. Unusually strong wind gusts, exceeding 100 miles per hour, spread the fires throughout LA, scattering flames across many communities. Climate change also intensifies fire smoke, filling the air with hazardous pollutants, which has negative health effects.

In California, the increasing frequency and severity of wildfires have increased disaster costs, causing insurers to raise premiums or deny policy renewals. California’s home insurance rates rose by 48.4 percent between 2019 and 2024. Twelve major insurers have also restricted homeowners insurance even after being granted large rate hikes.

Insurers have justified abandoning California homeowners by citing rising climate risk, yet they are complicit in facilitating climate change through their massive investments in fossil fuel related assets – including coal, oil, and gas – the primary sources of the greenhouse gases driving climate change.

State Farm’s Hypocrisy

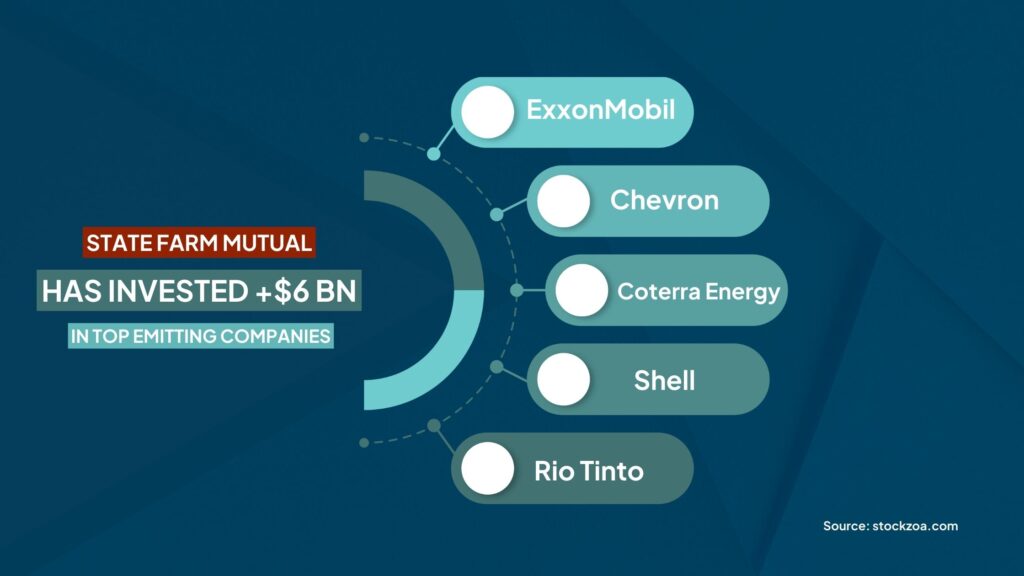

State Farm General (State Farm), through its parent company, State Farm Mutual, represents a major investor in fossil fuels. The company’s investments encompass over $6 billion in upstream oil and gas producers ExxonMobil, Chevron, Coterra Energy, and Shell, as well as the mining company Rio Tinto. These five companies are among the top investor-owned entities with the highest historical carbon dioxide emissions.

State Farm Mutual also holds billions of dollars in investments in fossil-fuel-intensive or dependent industries such as utilities, oil and gas services, and pipeline companies, as well as chemical, steel, and fertilizer manufacturers.

Despite facilitating climate change, State Farm – the largest property and casualty insurer in California – announced in 2023 that it would not renew 30,000 home insurance policies in the state. This decision was primarily attributed to the rising risk of wildfires in California.

Following an approved rate increase of 20 percent in December 2023, among other concessions from the California Department of Insurance, State Farm agreed to renew these 30,000 home insurance policies, but only under the condition that these renewed policies would exclude fire coverage. State Farm clients had to specifically secure separate fire coverage from the FAIR Plan. The exclusive Palisades, where many homes burned, was one of the areas in which State Farm significantly reduced its coverage. According to California Department of Insurance spokesperson Michael Soller, State Farm dropped about 1,600 policies in Pacific Palisades in July.

State Farm also discontinued over 2,000 policies in other LA zip codes, including neighborhoods also severely damaged by the wildfires, specifically Brentwood, Calabasas, Hidden Hills, and Monte Nido. The FAIR Plan is now the primary source for wildfire coverage for former State Farm policyholders.

State Farm: Reinsurance Profits and Rate Hikes

Most private insurers rely on their reinsurer to cover their losses from the LA Fires. Reinsurance, essentially insurance for insurance companies, is a standard part of an insurer’s business model, allowing them to transfer some of their risk to protect themselves from the most catastrophic events.

State Farm’s reinsurer is its parent company – State Farm Mutual. From 2014 to 2023, State Farm paid reinsurance premiums of nearly $2.2 billion but only received $0.4 billion back – less than 20 percent – implying the company overpaid for reinsurance. These payments to its parent company, with a low return, sparked accusations that State Farm was artificially boosting its parent company’s profits.

State Farm Mutual has over $130 billion in surplus available to support its subsidiary. Despite the exorbitant profits of its parent company and well before the LA Fires, in June 2024, State Farm requested a 30 percent increase in its homeowners insurance rates (on top of the 20 percent increase it was granted in March of the same year) purportedly to improve its general financial condition. Within days of the LA fires being contained, State Farm again asked its California policyholders to step in and maintain the profits of its parent company.

State Farm requested an annual $740 million bailout in the form of an “urgent” 22 percent increase in State Farm’s home insurance rates, along with requests for rate hikes of 38 percent for rental dwellings and 15 percent for tenants. Fortunately for California’s consumers, Commissioner Ricardo Lara rejected State Farm’s requested rate increase.

As well as reducing its exposure to climate change-induced wildfires, State Farm attempted to reduce it further, effectively requesting policyholders to take on more of the remaining risk. All the while, they continue to facilitate climate change and profit from their fossil fuel investments.

The FAIR Plan: Fighting for Survival

As insurance companies withdraw from vulnerable areas or increase premiums, many California homeowners are forced to depend on the FAIR Plan – the state-supported insurer of last resort. The FAIR Plan provides limited coverage at elevated rates, making it costly and an insufficient safety net for homeowners abandoned by private insurance companies.

The exodus of insurers from the California residential property market has exponentially increased the FAIR Plan’s exposure to wildfire risk. The FAIR Plan currently holds 13,752 policies with over $23 billion in liability across the residential and commercial sectors in the zip codes affected by the fires.

On February 11, 2025, Insurance Commissioner Lara determined “that the FAIR Plan is faced with a substantial threat of insolvency due to unprecedented losses” and approved the FAIR Plan’s request to levy an assessment totaling $1 billion on private insurance companies. Before July 2024, insurers operating in California would have been solely burdened with funding any deficit, paying a fee based on their market share.

However, a July 2024 regulation permits insurers to shift 50 percent of the assessment onto the state’s existing policyholders. Homeowners throughout California are being asked to bail out the FAIR Plan, irrespective of the risk profile of their home and neighborhood, and the climate risk mitigation or adaptation they have undertaken. This regulatory change was part of a series of concessions Lara has given to the insurance industry in recent years.

Holding the Real Culprits Accountable

Insurance companies enable climate change by investing in fossil fuel assets and underwriting fossil fuel projects. Nonetheless, the primary drivers of climate change are the fossil fuels themselves, and it is the companies that produce and sell them that are principally responsible for the climate emergency. Instead of shifting their exposure to California’s residents, insurers should divest from fossil fuel assets and cease underwriting fossil fuel projects.

Insurers should seek to recoup the costs of covering climate change-induced storms from fossil fuel companies – not from the individual policyholders or the public at large. A new bill, SB222, now before the California legislature, would make it easier to ensure that polluters pay for the climate-driven disasters befalling residents and upending the insurance industry. It specifically directs the FAIR Plan and incentivizes private insurers to pursue the parties responsible for climate change-induced weather events by standing in the shoes of policyholders to recoup the costs of losses, utilizing their right of subrogation.

An insurer’s right of subrogation is the right to try to recover the amount of a claim or claims it paid out from another party that caused the insured loss(es). The draft legislation directs the FAIR Plan to exercise its right of subrogation against “a responsible party for a climate disaster or extreme weather or other events attributable to climate change” if the benefits of subrogation outweigh the costs (as determined by an independent advisory body).

If the FAIR Plan’s funds are exhausted and private insurance companies are being assessed, as is the case now, the Bill also provides incentives to insurers to exercise the right of subrogation against a “responsible party” for a climate disaster. An insurer’s share of the assessment will be reduced by 10% if the insurer exercises its right of subrogation against a responsible party, but it will increase by 10% if subrogation is not exercised.

Finally, in addition to its right of subrogation, the Bill provides that an insurer may seek damages against a responsible party for a climate disaster, extreme weather, or other events attributable to climate change. Make no mistake: the responsible parties driving climate change are fossil fuel businesses.

Conclusion

SB222 highlights that the fossil fuel sector is the real culprit of the climate emergency. But insurance companies are far from innocent bystanders. Insurers must stop enabling “business as usual” in the fossil fuel sector and stop facilitating the escalating climate crisis that causes climate change-induced events like the LA fires. Insurers’ conduct, when coupled with representations around protecting policyholders from peril and justifications for rate hikes and non-renewals, violates consumer protection laws and standards.

Insurers must no longer be permitted to invest large portions of premium income in fossil fuel companies and underwrite new oil and gas projects while charging some homeowners more for increased climate risk and turning others away. Before any further handouts are given to the insurance industry or any more concessions are made to preserve a profit-driven insurance model that may simply be untenable in the age of climate chaos, insurers must stop fanning the flames.