In 2023, the property and casualty (P&C) insurance sector saw significant activity across the United States, with direct premiums earned varying widely by state. California led the nation, raking in a staggering $88.1 billion. Texas and Florida followed, with $70.9 billion and $63.8 billion, respectively. These three states also have the highest number of P&C insurance agents, reflecting the substantial premium volumes generated.

However, a closer look reveals that premium volume isn’t the whole story. When considering the estimated premium per agent, the rankings shift dramatically. Montana, with the fewest P&C agents, tops the list, generating an estimated $3.6 million in premium per agent. Alabama and Arkansas follow, with $3.1 million and $2.8 million, respectively. Ohio presents a contrasting picture, registering the lowest premium per agent at just $592,920.03. This data suggests that Montana may be the most lucrative U.S. state for insurance agents in terms of premium generated, while Ohio is the least.

Montana’s high premium per agent can be attributed to a relatively small population (roughly 1.1 million), which translates to fewer agents. Furthermore, the state’s economy and environment result in policies that tend to have higher premiums. Industries such as agriculture, ranching, and natural resources, which are prevalent in Montana, often necessitate more expensive insurance coverage. In addition, Montana has some of the highest auto insurance rates in the country, mainly due to long, rural highways prone to accidents, high rates of uninsured motorists, and the added cost of repairing larger vehicles, making the state a riskier area for insurers.

Conversely, Ohio’s position at the bottom of the premium-per-agent ranking stems from a different set of factors. The state has a high concentration of insurance companies and agents, driving intense competition that subsequently lowers premiums. Major insurance companies such as Progressive, Nationwide, and Cincinnati Insurance are headquartered in Ohio, increasing efficiency and reducing costs. Car insurance rates in Ohio are also consistently among the lowest in the nation, a result of a dense highway system with less severe accidents, competitive pricing, and lower numbers of uninsured drivers. Moreover, Ohio’s monopolistic state fund for workers’ compensation helps control pricing.

Across the U.S., statistics show a total of 2,412,480 registered insurance agents. Nearly 40% of these agents are concentrated in three states: Texas, Florida, and California—the three most populous states. Florida leads with 369,938 insurance agents, followed by Texas with 354,661, and California with 189,035. It is noteworthy that, although California is the most populous, it has fewer registered insurance agents than both Texas and Florida, with almost half as many registered in California as in Florida,

This disparity may be partially explained by Texas and Florida’s lack of state income tax, making them more attractive for agents and agencies seeking to maximize their earnings. Beyond their population size, these three states are also prone to natural disasters, including hurricanes in Florida, tornadoes in Texas, and wildfires in California. These events drive an increase in insurance demand, which in turn requires more agents to handle policies, claims, and risk assessment.

At the other end of the spectrum, Alaska has the fewest insurance agents, with 2,138, followed by Montana with 2,503 and Wyoming with 3,061.

The gender distribution among insurance agents in the U.S. is slightly male-dominated, with males comprising 44.83% of the agent population, while females represent 39.08%. The remaining 16.09% comprises agents who didn’t register as either male or female. While males make up less than half of the U.S. agent population, most states have more male agents than female. Only seven states—Texas, Georgia, Nevada, Mississippi, Hawaii, Wyoming, and Alaska—report a higher number of female agents.

The U.S. insurance market sees a considerable presence of young professionals, with 43% of agents having between zero and five years of experience. With longer tenure, the number of agents declines, with only 10% possessing 25 or more years of experience. However, California and Vermont stand out as exceptions to this trend, as they are the only two states where the majority of agents have between six and 15 years of experience. California boasts one of the largest and most intricate insurance markets in the nation, a result of a large population, a diverse economy, and significant regulatory demands, and as a result, highly experienced agents are in demand. The demand is particularly high in commercial lines, high-value home insurance, and specialized coverage such as wildfire and earthquake insurance.

Despite a large number of young professionals in the industry, those over 36 dominate the market. However, a significant percentage of agents (52.8%) did not register their age, which means this part of the data only paints half the picture.

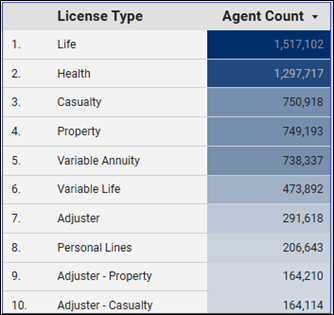

In terms of license type, life insurance leads the way, making it the most common license held by agents, followed by health, casualty, and then property. Life insurance is the most popular because of its broad customer base, high commission potential, and ease of licensing. Health insurance follows due to regulatory demands and recurring policy renewals, while casualty and property insurance require more technical expertise, making the licensing process more complex and resulting in these licenses being less common among agents.