Tech Reshaping How People Manage Their Insurance

The insurance sector is undergoing a significant transformation driven by technological advancements, particularly in telematics-based car insurance and the rapidly expanding cyber insurance market.

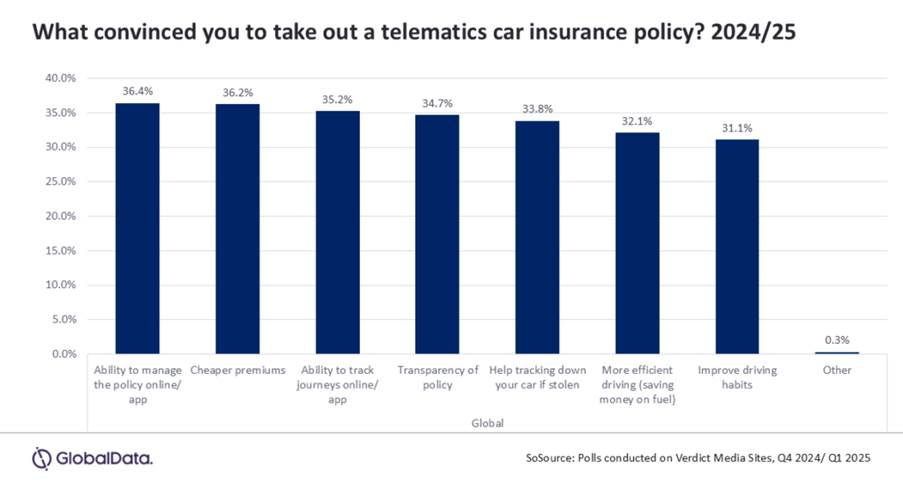

Telematics: A New Era in Car Insurance

Consumer demand for digital management, cost savings, and increased transparency is fueling the rise of telematics-based car insurance policies. A recent survey conducted by GlobalData on Verdict Media sites during late 2024 and early 2025 revealed that 36.4% of respondents were motivated to adopt a telematics policy due to the ability to manage their policy online or via a mobile app. Another 36.2% of those surveyed cited cheaper premiums as the primary reason for switching to telematics. Other influential factors included the convenience of online journey tracking (35.2%), policy transparency (34.7%), assistance in locating stolen vehicles (33.8%), and the potential for savings through more efficient driving habits (32.1%). Moreover, over 30% of policyholders were drawn to telematics for its ability to improve driving behavior.

Digitalization: The Driving Force Behind Market Shifts

The increased integration of technology extends to sectors such as cyber insurance.

According to GlobalData, the cyber insurance market in the UK is poised for double-digit growth, with an anticipated 44.7% expansion in 2024 and a projected compound annual growth rate (CAGR) of 27.7% from 2023 to 2028. Despite the sector’s rapid expansion, insurers face challenges in accurately assessing cyber risk due to the limited availability of historical data and complexities of containing exposure.

A separate poll of 105 industry insiders conducted by GlobalData showed that accurately assessing risk is the primary concern for insurers providing cyber coverage. Other key challenges include managing claims and the limitations in reinsurance options, especially as cyberattacks become increasingly more sophisticated.

“Cyber insurance differs from other lines, such as household coverage, where insurers could limit the number of properties covered in high-risk areas,” noted Ben Carey-Evans, a senior insurance analyst at GlobalData. “This creates a careful balance between growing the product and keeping premiums low to attract customers, especially as the level of risk escalates.”